AICredit

Next.js-based credit decision platform. It unifies ONNX/WASM inference, the Home Credit data pipeline, threshold analysis, and dashboard-driven decision support screens into one product.

Overview

I designed AICredit not as a single-screen credit scoring demo, but as an

operations product that manages the decision process end to end. At its core

sits an ONNX/WASM inference pipeline running in the browser; around it, I tied

application operations, individual record review, the simulator, data

transparency, and model performance auditing into the same product language.

The goal was never just to produce a score, but to make visible how that score

is used and within which workflow.

On the model side, a v3.0.0 distilled architecture using 60 features,

together with an AUC of 0.8007 and a GINI of 0.6014, powers the product's

decision engine. The data layer pulls in the Home Credit pipeline, scored

applications via application_master.csv, and Neon-backed endpoints. On the

interface side, Next.js, TypeScript, Recharts, and an animated bento

layout deliver a dark, high-contrast decision support experience.

AI-powered decision support system that brings credit risk scoring, model analytics, and scenario simulation into a single dashboard product.

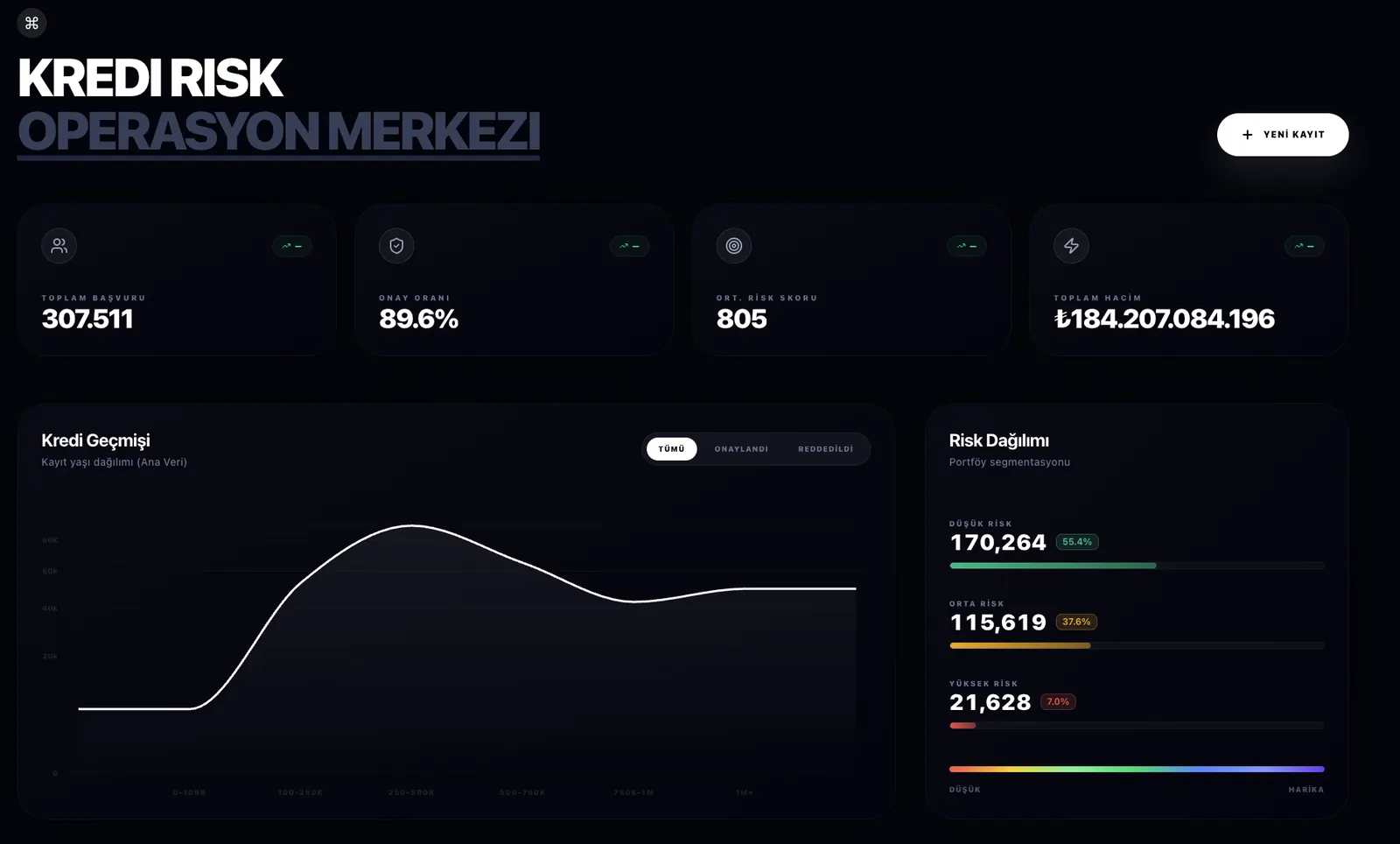

Operations center

The first screen gives an overview of the risk operation. Top-level KPIs such as total applications, approval rate, average risk score, and total volume read at a glance. Below them, the distribution of credit history sits alongside risk segmentation on the same panel, so the operations team sees not just numbers but the composition of the portfolio in an instant.

The point of this screen isn't to show off a slick dashboard; it's to translate the scoring result into a daily decision rhythm. In other words, the model output turns directly into operational follow-up.

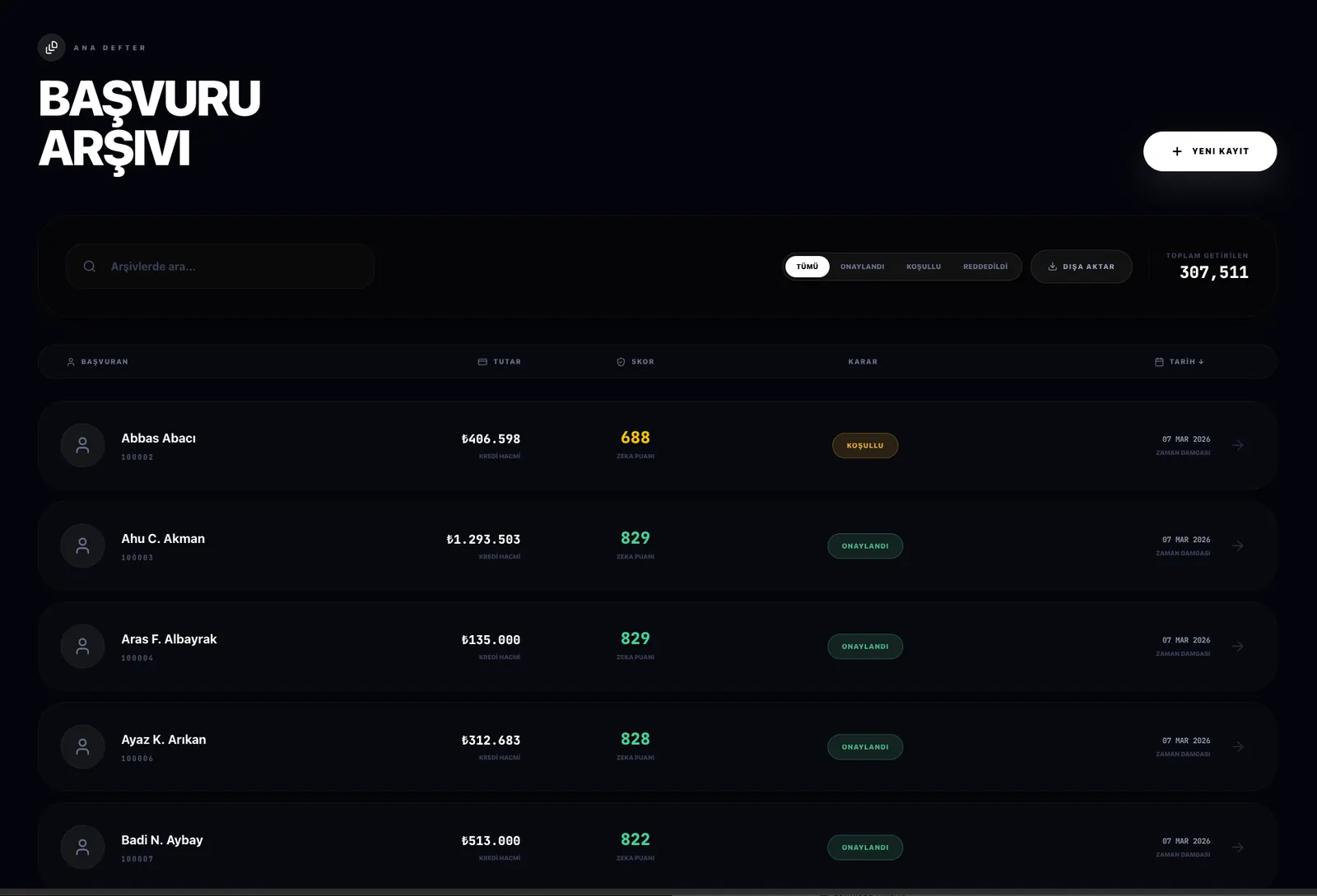

Application archive

The second layer is the operational triage screen. Applications are listed in an archive layout with score, decision, amount, and timestamp. Thanks to filters and quick search, the team isn't just reading a report; they can navigate the active application pool and inspect the decision set in real time.

Bold typography, clean decision labels, and dark surfaces keep readability intact even as data density climbs.

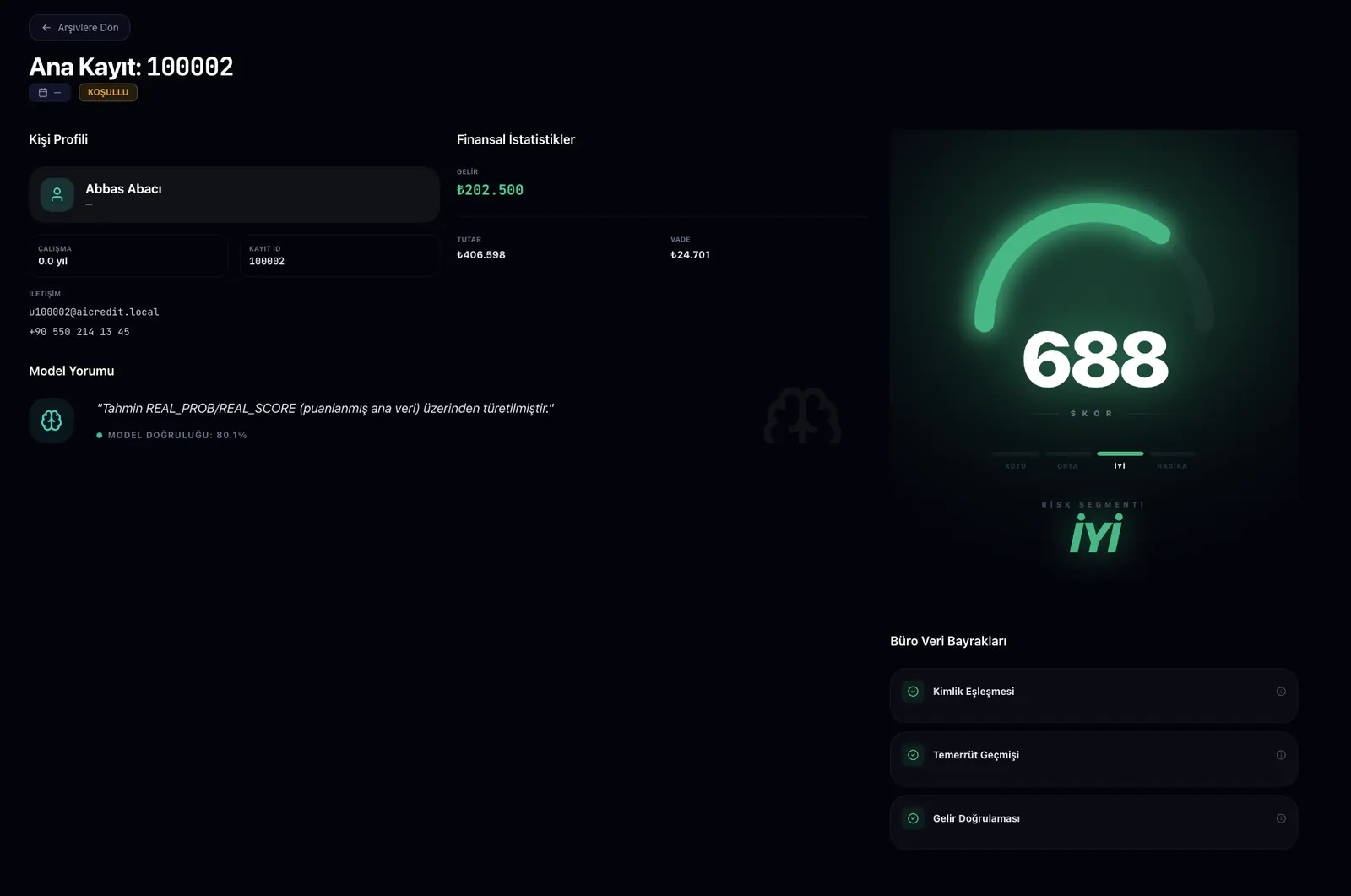

Individual record review

To show why a given application received a particular score, the record detail page was designed as a dedicated decision review surface. The applicant profile, financial statistics, model commentary, score gauge, and bureau flags all come together on one screen. This lets the operations team answer the question "where did this score come from?" in a single view.

This page matters in particular because, in model-driven products, the trust problem usually arises not from the prediction itself but from a lack of explanation. Here, the score is shown together with its context.

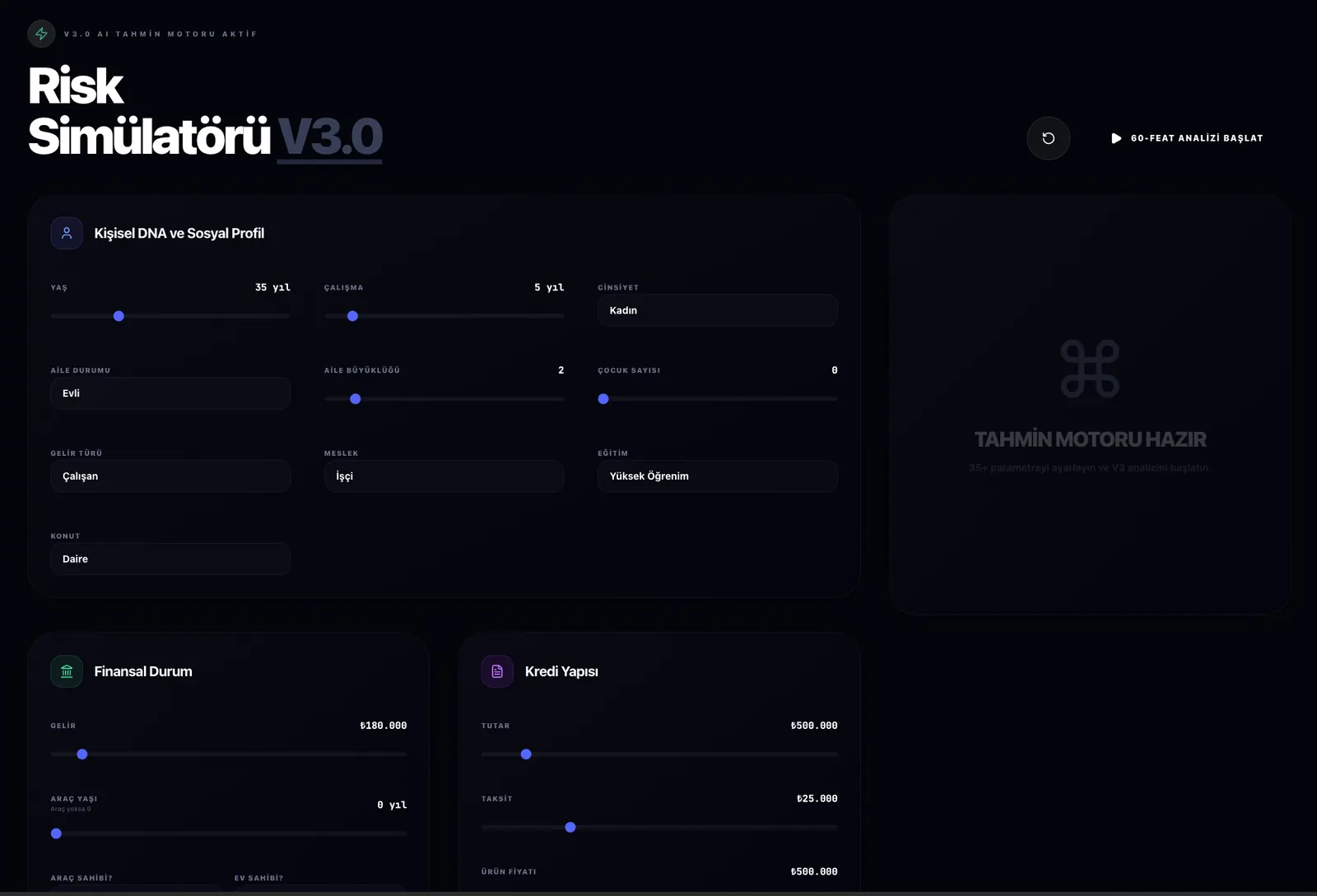

Risk simulator

One of the most valuable aspects of the product is its ability to step out of static scoring logic and into scenario analysis. On the simulator screen, age, income, credit structure, bureau summary, and external signals can be changed to re-run the 60-feature inference engine. This way, a credit specialist doesn't just review a new record; they can experiment with possible decision shifts.

This layer turns the model from a passive analysis tool into an active decision laboratory. From a product standpoint, it's one of the real differentiators.

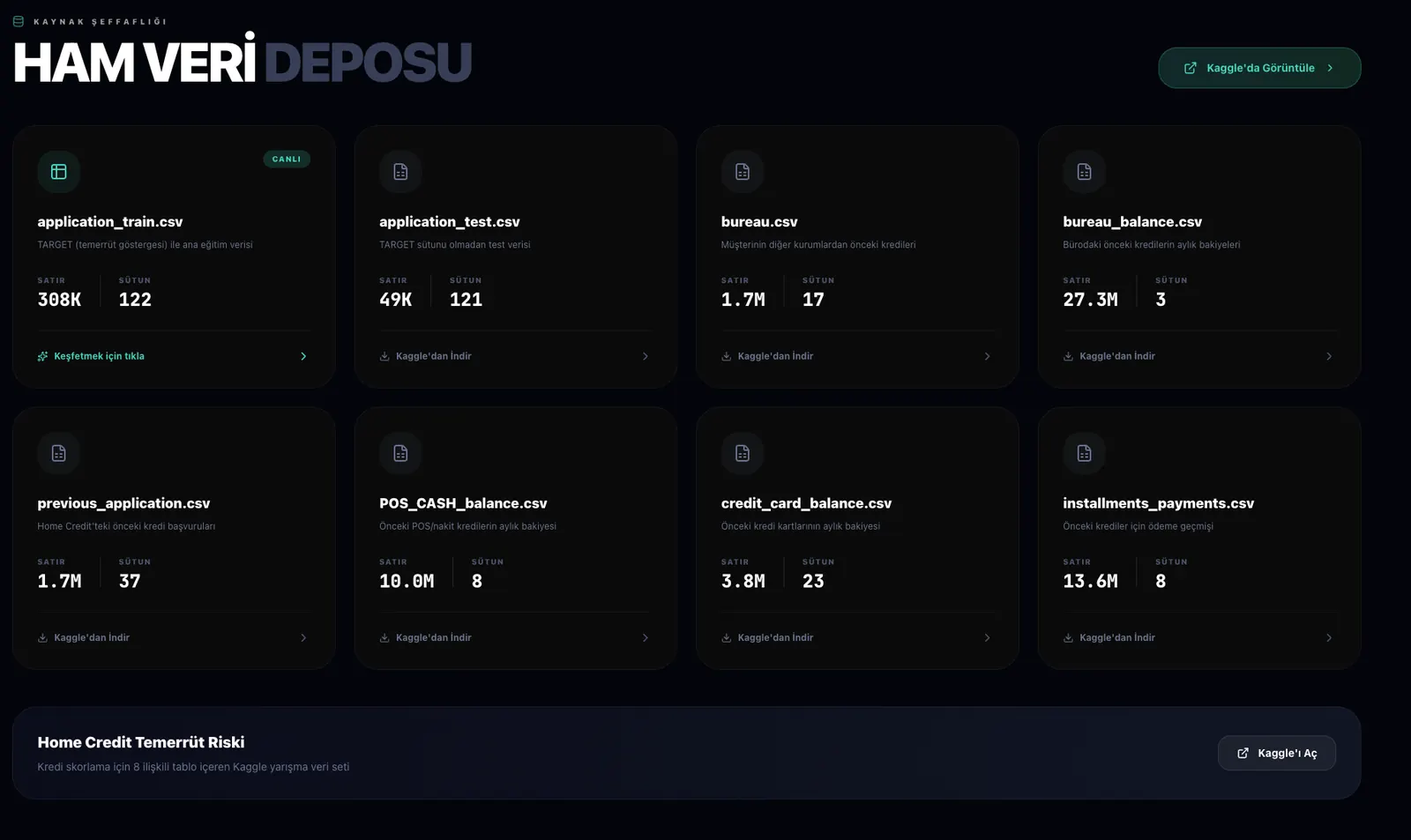

Raw data store

I made data transparency part of the product as well. The core tables in the Home Credit dataset are listed in a separate catalog screen, along with their row and column scales. This area makes the data feeding the scoring system visible, opening up the relationship between the model and its source data for the user.

With this approach, the project isn't just a panel that shows "the result"; the database and the table family the result is derived from become part of the product too.

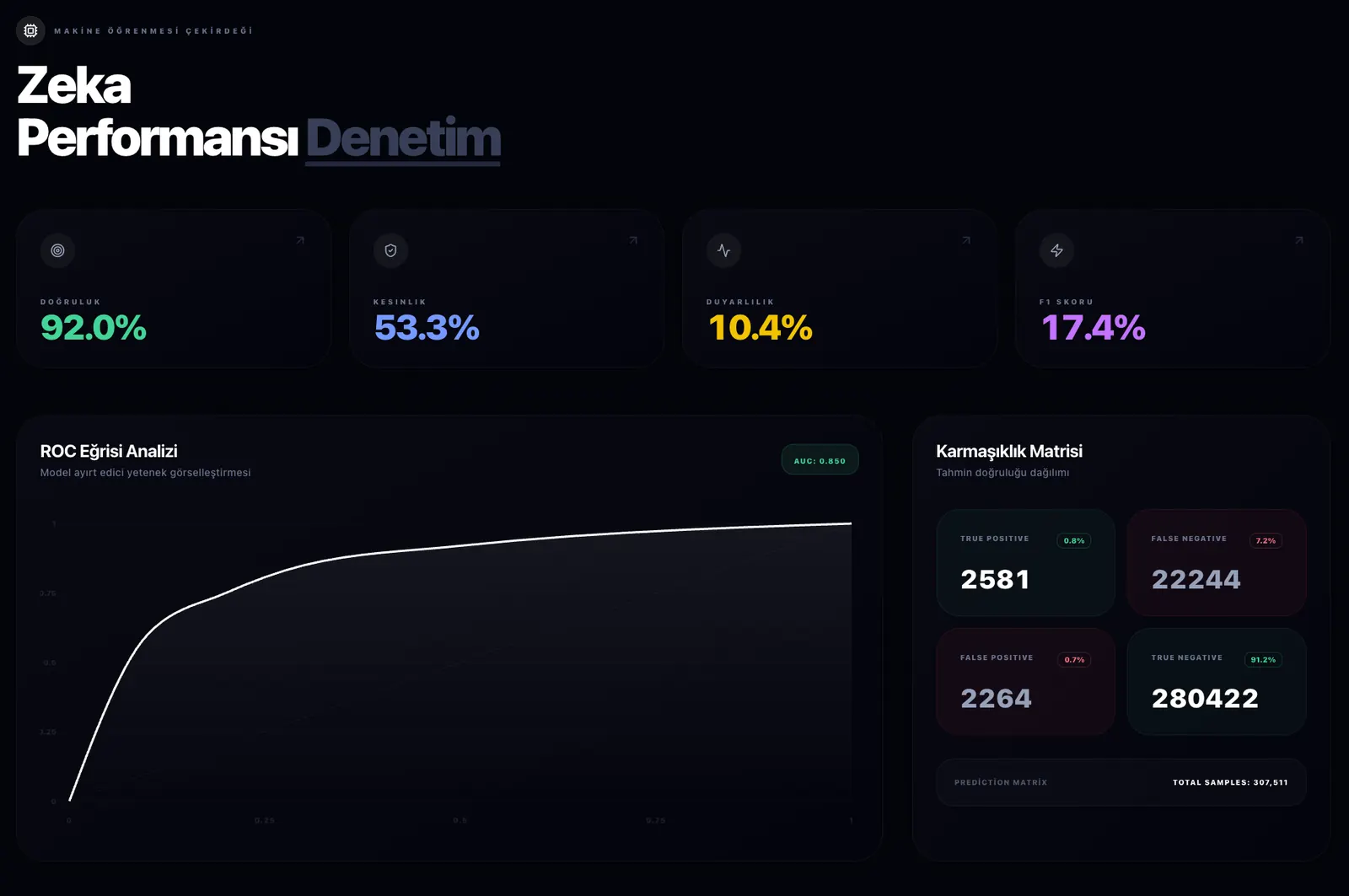

Model performance auditing

Quality control on the model side was also handled as a separate screen. The ROC

curve, confusion matrix, and metrics like accuracy / precision / recall / F1 are

brought together on a single audit page. This goes beyond showing top-level

results such as AUC 0.8007 and makes model behavior operationally trackable.

The goal here wasn't to build a metrics board only a data scientist would look at; I wanted a product manager or operations owner to be able to understand model health too.

Conclusion

In the end, AICredit grew into more than a one-off credit prediction demo. With a

decision engine powered by ONNX Runtime Web, a Neon-backed data pipeline, and

the operations dashboard, archive, individual record, simulator, data catalog,

and analytics layers, it delivers a complete credit risk operations experience.

That's why I position the project not just as an ML application, but as an

enterprise decision support system that unifies the model and the workflow in a

single product.

Highlights

Technical Architecture

CoreInsight

FastAPI- and Next.js-based Text-to-SQL + BI copilot system. It turns natural language queries into safe SQL and the results into charts and analysis.

BI Copilot System